Accidents happen; that’s why they’re called accidents. And they can happen to anyone at any time, resulting in everything from a broken arm to a broken back – or worse. After a serious injury occurs, most people immediately focus on treatment and recovery. However, once the initial shock wears off, their thoughts may turn to finances.

Accidents happen; that’s why they’re called accidents. And they can happen to anyone at any time, resulting in everything from a broken arm to a broken back – or worse. After a serious injury occurs, most people immediately focus on treatment and recovery. However, once the initial shock wears off, their thoughts may turn to finances.

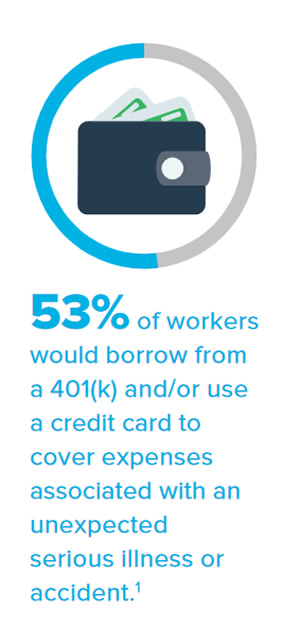

According to the 2017 Aflac WorkForces Report, 53 percent of workers would borrow from a 401(k) and/or use a credit card to cover expenses associated with an unexpected serious illness or accident.1 Fortunately, accident insurance can help.

Voluntary accident insurance helps employees cope with out-of-pocket costs associated with serious accidents — costs major medical insurance may not cover. In the event of a covered incident, accident insurance provides cash benefits directly to the policyholder that can be used in any way they see fit (unless otherwise assigned). It can help workers and their families stay ahead of the medical and out-of-pocket expenses that add up so quickly after an injury, including treatment-related costs and everyday bills that continue to roll in.

Depending on the policy, accident insurance typically pays a specific benefit amount for:

In addition, some policyholders may select an optional accidental death benefit rider, which pays a lump-sum death benefit for covered common-carrier accidents and other accidents.

It’s important to note that health exams aren’t required to qualify for voluntary accident insurance. If an employer offers a voluntary accident plan, workers may receive payroll rates and have premiums deducted from their paychecks.

Unlike some insurance policies that may be more appropriate for certain age groups or at-risk individuals, voluntary accident coverage may be beneficial to most employees because it helps provide financial protection from covered accidents.

Voluntary accident coverage helps provide financial confidence for workers and their families. Even those with comprehensive major medical plans in place may find that out-of-pocket costs stemming from an accidental injury can be substantial. In addition, 72 percent of employees who are not offered voluntary insurance at work would be at least somewhat likely to purchase it if offered.1

Voluntary accident coverage helps provide financial confidence for workers and their families. Even those with comprehensive major medical plans in place may find that out-of-pocket costs stemming from an accidental injury can be substantial. In addition, 72 percent of employees who are not offered voluntary insurance at work would be at least somewhat likely to purchase it if offered.1

Even the most minor of accidents, such as a broken arm, can lead to temporary loss of income and inability to pay normal living expenses. Regular bills, including the mortgage or rent, car payments and utility bills, don’t stop when an individual is unable to work after an injury. The protection accident insurance helps provide can allow policyholders and their families to focus on recovery – not on finances.

This article is for informational purposes only and is not intended to be a solicitation.

1The 2017 Aflac WorkForces Report is the seventh annual study examining benefits trends and attitudes. The study’s surveys, conducted by Lightspeed, captured responses from 1,800 benefits decisionmakers and 5,000 employees across the United States in various industries. For more information, visit www.AflacWorkForcesReport.com.

In Arkansas, Policies A36100AR–A36400AR, & A363OFAR. In Idaho, Policies A36100ID–A36400ID, & A363OFID. In Oklahoma, Policies A36100OK–A36400OK, & A363OFOK. In Oregon, Policies A36100OR–A36400OR, & A363OFOR. In Pennsylvania, Policies A36100PA-A36400PA. In Texas, Policies A36100TX–A36400TX, & A363OFTX. This is a brief product overview only. Coverage may not be available in all states. Benefits/premium rates may vary based on plan selected. Optional riders are available at an additional cost.The policy has limitations and exclusions that may affect benefits payable. Refer to the policy for complete details, limitations, and exclusions.

Coverage is underwritten by American Family Life Assurance Company of Columbus. In New York, coverage is underwritten by American Family Life Assurance Company of New York.

Z171458

EXP 10/18