Advances in medicine mean people today live longer lives, even if they suffer from critical illnesses. Naturally, living longer with a critical illness may mean paying more treatment related costs – a possibility that has many Americans concerned. According to a Sun Life Financial study, many workers fear the financial impact of a critical illness even more than dying from one.1

As a benefits decision-maker, you understand the importance of critical illness coverage. And while most workers are well-versed about the need for major medical, home and vehicle insurance, many don’t know that critical illness coverage exists. Voluntary critical illness insurance is a way for employees to help themselves stay ahead of the medical and out-of-pocket expenses that can accompany certain medical events. For example, many lump-sum critical illness policies pay benefits when an individual experiences a covered event such as:

Critical illness coverage helps provide protection from the financial impact of certain catastrophic health events. Receiving a lump-sum benefits payment can help policyholders worry less about how to pay illness-related expenses and concentrate more on recovery.

With new statistics and projections about the likelihood of suffering from a critical illness, there has never been a better time to offer voluntary insurance at the work site. As employers evaluate, choose and communicate their benefits offerings to employees, it is important they convey the potential financial impact of being diagnosed with a critical illness.

The 2017 Aflac WorkForces Report survey revealed that health care costs have a long-lasting effect on American workers’ creditworthiness. Over half of participating employees said medical costs are affecting their credit scores, keeping them from paying other bills and thwarting their efforts to save for retirement or a rainy day. The survey revealed that 65 percent of American workers have less than $1,000 on hand to pay out-of-pocket expenses associated with an unexpected serious illness or accident. What’s more, 53 percent would borrow from a 401(k) and/or use a credit card to cover out-of-pocket expenses if they or a family member experienced an unexpected serious illness or accident.2

The 2017 Aflac WorkForces Report survey revealed that health care costs have a long-lasting effect on American workers’ creditworthiness. Over half of participating employees said medical costs are affecting their credit scores, keeping them from paying other bills and thwarting their efforts to save for retirement or a rainy day. The survey revealed that 65 percent of American workers have less than $1,000 on hand to pay out-of-pocket expenses associated with an unexpected serious illness or accident. What’s more, 53 percent would borrow from a 401(k) and/or use a credit card to cover out-of-pocket expenses if they or a family member experienced an unexpected serious illness or accident.2

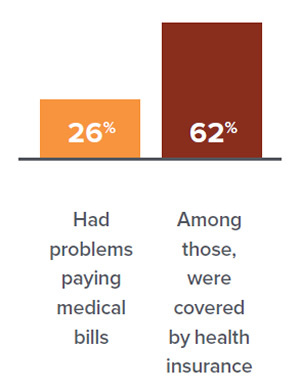

The Aflac report’s findings are echoed by those of the Kaiser Family Foundation, which found that one-quarter (26 percent) of U.S. adults ages 18-64 say they or someone in their household had problems paying or an inability to pay medical bills in the past 12 months. The study also found that among all people with household medical bill problems, more than 62 percent say the person who incurred the bills was covered by health insurance.3

The Aflac report’s findings are echoed by those of the Kaiser Family Foundation, which found that one-quarter (26 percent) of U.S. adults ages 18-64 say they or someone in their household had problems paying or an inability to pay medical bills in the past 12 months. The study also found that among all people with household medical bill problems, more than 62 percent say the person who incurred the bills was covered by health insurance.3

In addition to playing havoc with employees’ finances, the high price tag of critical illness affects companies’ bottom lines. The financial distress suffered by workers can lead to absenteeism, on-the-job distraction and a general sense of anxiety that is difficult to leave at the door.

When working with a broker or insurance advisor to strengthen their organizations’ benefits offerings, human resources experts should ask for information about how critical illness insurance fits into the picture. In general, critical illness policies work side by side with major medical plans by offering cash benefits that can be used to help with deductibles, copayments and other out-of-pocket medical costs. Because cash benefits can be used as policyholders see fit, they can also be used to help with household expenses, including the rent or mortgage, utilities, credit card debt and any other bill.

When working with a broker or insurance advisor to strengthen their organizations’ benefits offerings, human resources experts should ask for information about how critical illness insurance fits into the picture. In general, critical illness policies work side by side with major medical plans by offering cash benefits that can be used to help with deductibles, copayments and other out-of-pocket medical costs. Because cash benefits can be used as policyholders see fit, they can also be used to help with household expenses, including the rent or mortgage, utilities, credit card debt and any other bill.

This article is for informational purposes only and is not intended to be a solicitation.

1 Sun Life Financial. “Well-placed fears: Workers perceptions of critical illness,” accessed Sep. 25, 2017 – http://www.sunlife.com/us/News+and+insights/Press+releases/Archives/2013/ci.Sun+Life+Financial+Report+Reveals+Workers+Concern+for+Costs+of+Critical+Illness.mobile?vgnLocale=en_CA..

2 The 2017 Aflac WorkForces Report is the seventh annual study examining benefits trends and attitudes. The study’s surveys, conducted by Lightspeed, captured responses from 1,800 benefits decision-makers and 5,000 employees across the United States in various industries. For more information, visit www.AflacWorkForcesReport.com.

3 Kaiser Family Foundation, "The burden of medical debt," accessed Sep. 25, 2017 - https://kaiserfamilyfoundation.files.wordpress.com/2016/01/8806-the-burden-of-medical-debt-results-from-the-kaiser-family-foundation-new-york-times-medical-bills-survey.pdf.

In Arkansas, Policies A73100AR and A7310HAR. In Idaho, Policies A73100ID and A7310HID. In New York, Policy NY72100. In Oklahoma, Policies A73100OK and A7310HOK. In Oregon, Policies A73100OR and A7310HOR. In Pennsylvania, Policy A73100PA and A7310HPA. In Texas, Policies A73100TX and A7310HTX. In Virginia, Policy A73100VA. This is a brief product overview only. Coverage may not be available in all states. Benefits/premium rates may vary based on plan selected. Optional riders are available at an additional cost. The policy has limitations and exclusions that may affect benefits payable. Refer to the policy for complete details, limitations, and exclusions.

Coverage is underwritten by American Family Life Assurance Company of Columbus. In New York, coverage is underwritten by American Family Life Assurance Company of New York.

Z171460